Daily Commentary

Commentary prepared by Alloya Investment Services, a division of the wholly owned CUSO of Alloya Corporate Federal Credit Union. Alloya Investment Services is a leading broker/dealer consultant to credit unions.

Monday, July 13, 2026 at 8:00 am CT

Commentary prepared by Tom Slefinger, Market Strategist

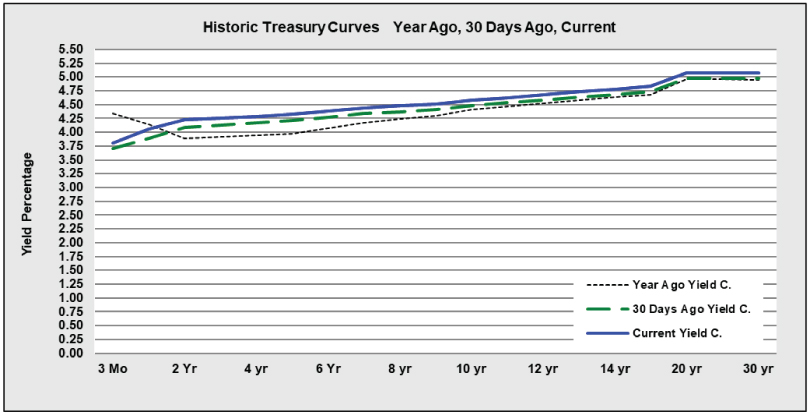

Market Indications

Other Market Indicators

| Market Indicators | ||

|---|---|---|

| 2s/5s Tsy Spread | 0.10 | 0.00 |

| 2s/10s Tsy Spread | 0.35 | 0.00 |

| 2s/30s Tsy Spread | 0.85 | +0.01 |

| DJIA-30 | 52,637.01 | +0.29% |

| S&P-500 | 7,575.39 | +0.42% |

| NASDAQ | 26,281.61 | +0.29% |

| Dollar Idx | 101.17 | +0.22% |

| CRB Idx | 467.90 | -0.63% |

| Gold | 4,061.00 | -1.22% |

Daily Commentary

Recap — Iran and the U.S. traded airstrikes again over the weekend, with the skirmishes continuing today. The escalation pushed oil prices higher and weighed on the risk-on trade. Tehran reportedly targeted U.S. facilities across several countries, including Kuwait, Bahrain, Oman and Jordan. They also declared the Strait of Hormuz closed. President Trump rejected that claim yesterday, saying the key waterway remained open to commercial traffic. Though, this was only after ordering retaliatory strikes following Iran’s attack on a commercial ship transiting the Strait. For more context, and in case you’re wondering who thinks they won the war, I suggest reading “How Trump Failed to Secure the Strait of Hormuz in His Iran Deal” from the New York Times, followed by this Wall Street Journal article, “Aspiring to Regional Domination, Iran Is Ready to Escalate Over Hormuz.” Brent crude climbed nearly 4% to roughly $79 per barrel on the latest flare-up.

For a more in-depth analysis on the economy and markets please read this week’s edition of the Weekly Relative Value — The New Golden Age — to be released later this morning.

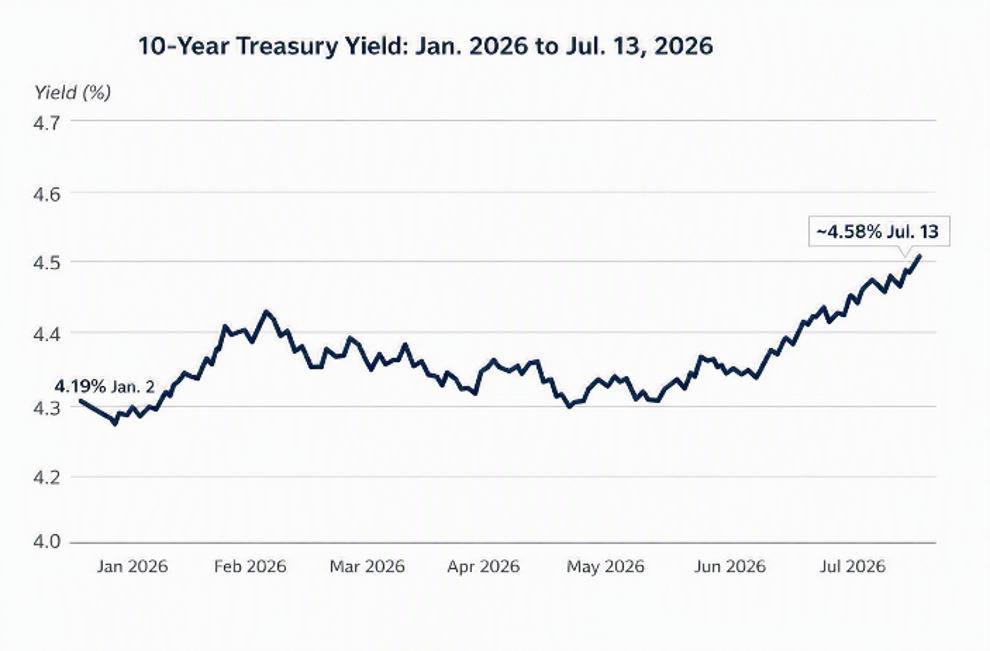

The yield on 10-year Treasury has hooked up +1 beep (4.57%) even as the futures market has decided that a Fed rate hike is a virtual fait accompli by the September FOMC meeting. Have a look at “War Leaves Economy with More Stubborn Inflation, Economists Project” and “Warsh’s First Big Call: Whether to Undo Last Year’s Cuts,” both in today’s Wall Street Journal.

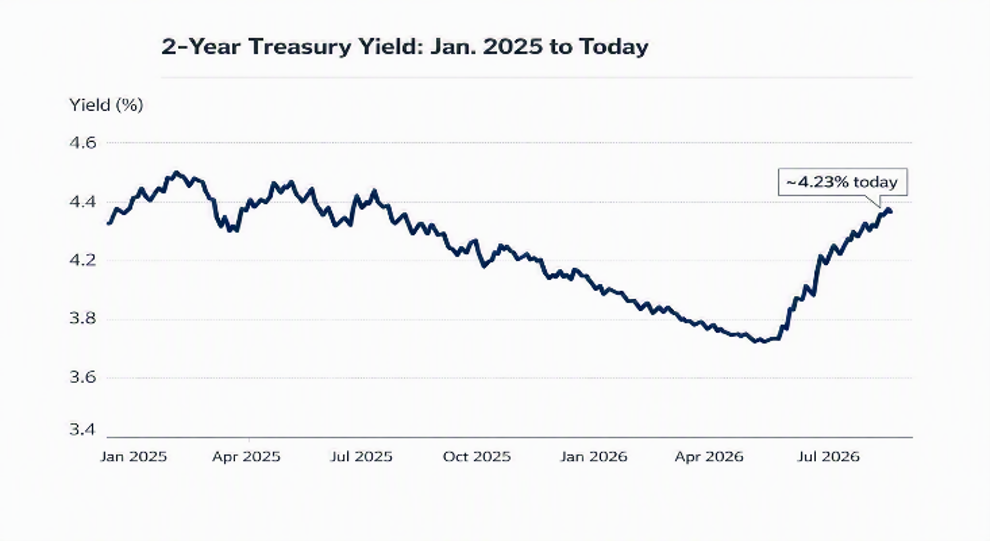

The yield on the 2-year Treasury note has shot up by more than +80 basis points since late February to over 4.2%, the same level it was trading at back in February 2025. It has been almost three years since we last saw such a spasm over such a short period of time. Keep in mind that despite what the bond market was pricing in back then, the next move by the Fed was to cut, not hike. However, the move is so extreme that the last time the 2-year Treasury note yield was this high, the Fed funds rate was sitting at 4.5% (upper end of the target). So, it is now safe to say that the front end of the curve has leapfrogged the Fed and is now pricing in not one but two rate hikes. This looks like late 2018 when the Fed tightened and sounded uber-hawkish. Then the next thing you know, it eased three times in 2019 without there even being a recession and the 2-year Treasury yield went from a peak of 2.98% to below 1.4% by the fall of 2019.

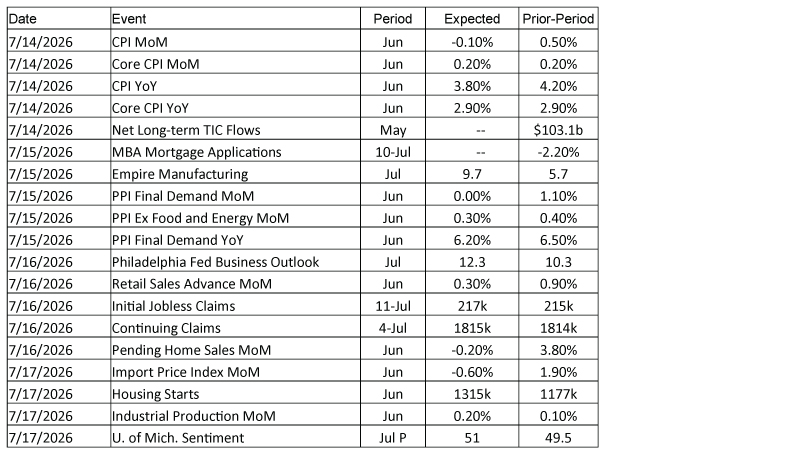

The next few days should be busy. Tomorrow, we have the June CPI report being released and Kevin Warsh’s first congressional testimony. This will be followed by the PPI report and the Fed’s Beige Book on Wednesday. Together, the price data should offer a solid read on the month’s PCE and core deflator.

Second quarter earnings season kicks off with 28 S&P 500 companies reporting — including JPMorgan Chase, Goldman Sachs, Morgan Stanley, Bank of America, Citigroup, Wells Fargo, Bank of New York Mellon, Regions Financial and Fifth Third Bancorp. We will also hear from Netflix, Johnson & Johnson and UnitedHealth.

For Treasury markets, Warsh takes center stage — even ahead of the data — since the reversal in oil prices should help contain CPI and PPI. Middle East developments remain a headline risk: The ceasefire is over, peace talks continue and oil is stuck in limbo. Under the interim deal, both sides have 60 days to reach a final nuclear agreement, though that deadline could be extended.

Stay tuned and have a great day!

Economic Calendar

July 13 - 17, 2026

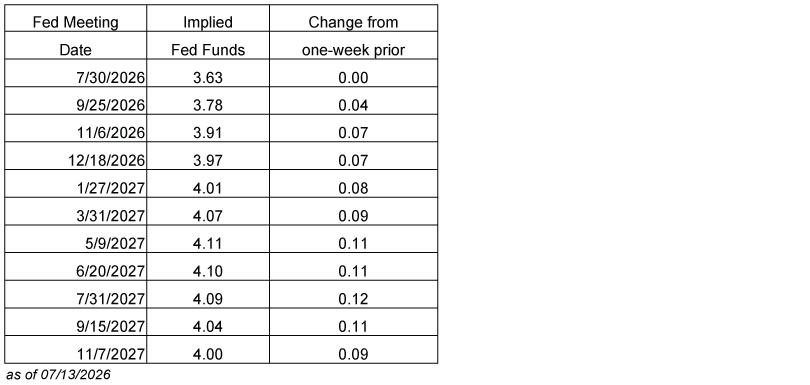

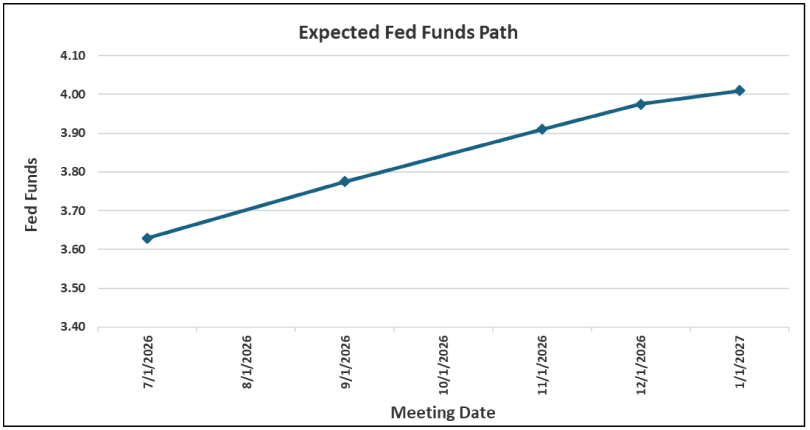

Future Fed Expectations

Source: Bloomberg

| Select Probabilities based on the Futures | |

|---|---|

| Probability of Fed Funds rate HIKE on July 29, 2026 | 24% |

| Probability of Fed Funds rate HIKE on September 16, 2026 | 43% |

**All quoted rates are indications and are subject to change without notice.

* ISI is a member of the FINRA/SIPC.

The information contained herein is prepared by ISI Registered Representatives for general circulation and is distributed for general information only. This information does not consider the specific investment objectives, financial situations or particular needs of any specific individual or organization that may receive this report. Neither the information nor any opinion expressed constitutes an offer, or an invitation to make an offer, to buy or sell any securities. All opinions, prices, and yields contained herein are subject to change without notice. Investors should understand that statements regarding future prospects might not be realized. Please contact Alloya Investment Services to discuss your specific situation and objectives.